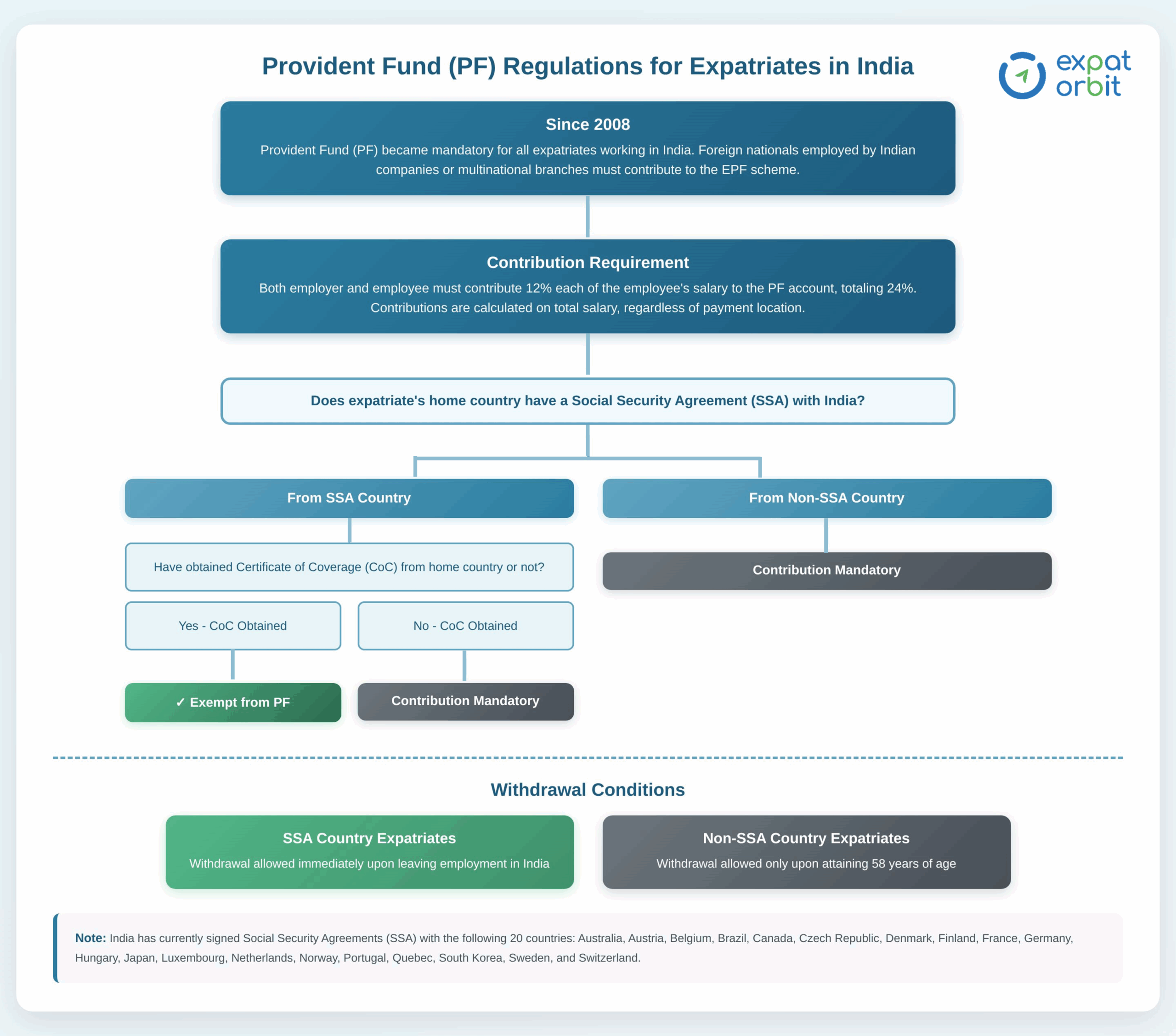

If an expatriate’s home country has a Social Security Agreement (SSA) with India, and the expatriate obtains a Certificate of Coverage (CoC) from their home country’s authorities, they are exempt from contributing to the Indian Provident Fund (PF). This exemption applies if the expatriate continues contributing to their home country’s social security scheme and submits the CoC as proof to the Indian employer and PF department. This typically occurs in secondment cases where the expatriate is transferred from a foreign parent or group company to its Indian affiliate. In such cases, the foreign entity remains responsible for social security contributions, and the expatriate is exempt from Indian PF upon submitting a valid CoC. Moreover, these expatriates are eligible to withdraw their PF balance immediately after completing their Indian assignment.

Provident Fund regulations apply only to establishments in India employing 20 or more individuals. Organisations with fewer than 20 employees are exempt from mandatory registration with the Employees’ Provident Fund Organisation (EPFO) and do not have to deduct or deposit PF contributions for any employee, including expatriates. This exemption generally covers small businesses, startups, new subsidiaries, and liaison offices that typically have limited headcount during their initial phases. While some smaller entities may choose voluntary registration and compliance, most do not, relieving expatriates working in such setups from mandatory PF deductions.

PF contributions are meant exclusively for ‘employees’ engaged under a formal employer-employee relationship, characterised by a regular salary and adherence to organisational supervision. Expatriates engaged as bona fide independent consultants, contracted on a service basis, remunerated via invoices or project fees, and lacking the typical employment benefits and controls are not subject to PF contribution requirements.

It is imperative to underscore that the distinction must be genuine; a consultancy arrangement cannot be a disguised employment contract to evade PF obligations; courts may look at substance over form if challenged.